The beverage alcohol industry faced a challenging February with both the wine and spirits sectors experiencing noticeable declines in volume and revenue. While a shorter month with one less shipping day contributed to the softer-than-expected performance, other market forces also played a role in shaping these trends.

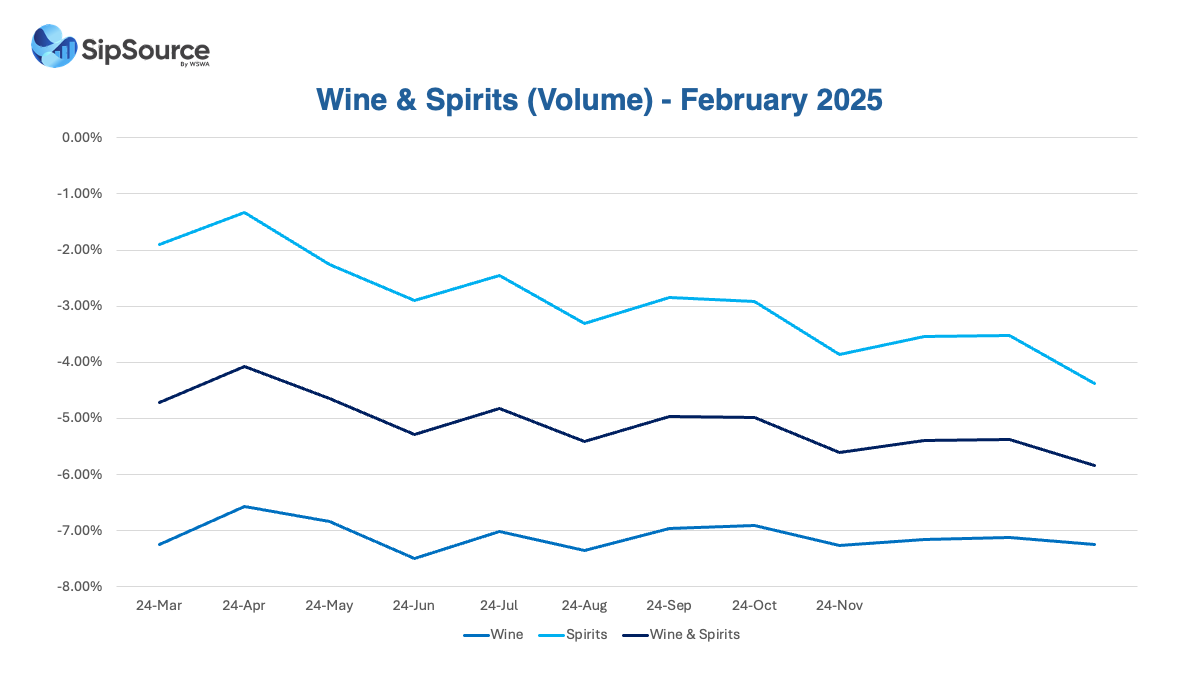

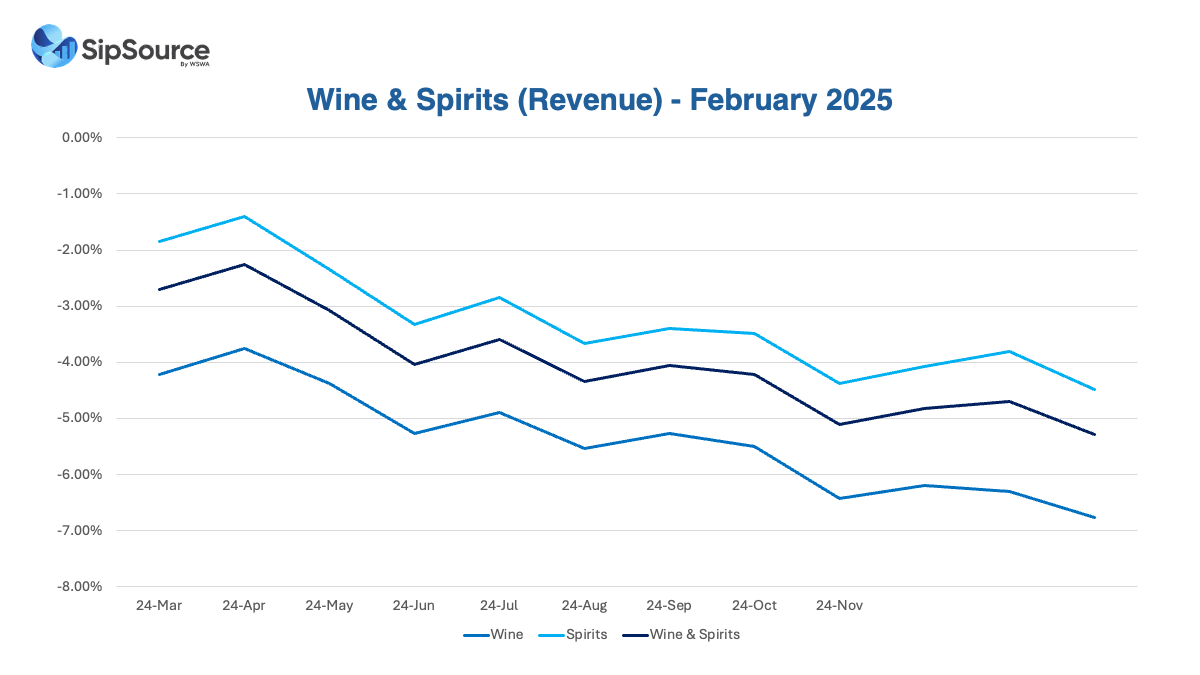

Declining Sales in Wine and Spirits

The wine industry continued to struggle, experiencing a -9.4% decrease in volume and a -10.8% drop in revenue. The sharper revenue decline compared to volume suggests increased pricing pressures, discounts, or lower-than-average selling prices affecting profitability.

The spirits segment saw a significant drop of -10.6% in volume and -9.4% in revenue for the month of February. This decline highlights the ongoing demand challenges in the sector, potentially driven by shifting consumer preferences, inflationary pressures, and economic uncertainties including potential tariffs on the imported spirits that make up 36% of the U.S. spirits marketplace.

Revenue-to-Volume Trend Shows a Mixed Picture

While overall sales declined, the revenue-to-volume trend revealed contrasting developments for spirits and wine. Spirits showed an improving trend, with a +250-basis point gain in January and an additional +120-basis point increase in February. This positive shift suggests that despite declining volumes, pricing strategies and premiumization efforts are helping stabilize revenue in the spirit’s market.

Conversely, the wine industry experienced a worsening trend in revenue-to-volume ratios, with a -50-basis point decline in January and a further -130-basis point drop in February. This decline underscores increased competition, pricing pressures, and shifting consumer preferences impacting the profitability of the wine segment.

Looking Ahead: March Trends Show Signs of Improvement

March comparisons appear more favorable, with expectations of an improvement in overall trends. The 2024 March comps are spirits declined by -10.5% in volume and -10.7% in revenue, while wine dropped -11.8% in volume and -10.8% in revenue. The timing of Easter in 2025, falling three weeks later on April 20th, may impact sales seasonality and demand fluctuations.

External Market Pressures Continue to Challenge Growth

Broader market conditions remain volatile, impacting consumer confidence and overall industry performance. Several factors are contributing to this uncertainty:

- Canadian boycott actions may hurt exports, with uncertain effects on domestic sales.

- Tariffs, inflation, and employment uncertainties continue to affect purchasing power.

- Retailers and on-premise operators are focusing on cash flow management and lowering inventory levels.

Will On-Premise Trends Stabilize?

After a difficult year in 2024, industry players are questioning whether on-premise sales trends will stabilize. Spirits have shown improvement over the past three months, and while wine volume is recovering, revenue challenges persist. To sustain momentum, beverage companies must continue to adapt their pricing strategies, monitor consumer trends, and navigate macroeconomic pressures effectively. The coming months will be crucial in determining the path forward for both spirits and wine sectors.